Groq: The Formula to Pick an AI Decacorn

Silicon Valley venture capital loves formulas.

Every VC today is optimizing their Sourcing and Winning “processes.” They build massive databases on every person who is (or could potentially be) a founder, run algorithms, race to find early momentum before competitors, and then try to demonstrate their potential value-add. Sourcing and Winning matter. But, today, especially with AI, they're just tablestakes.

The real alpha comes from Picking: recognizing what's non-obvious but correct, and having the conviction to act before consensus forms.

Picking isn’t about being the first to hear about a company. And it’s not about being the most aggressive when everyone already agrees. It’s about developing the judgment to actively seek out contrarian people and ideas, have a view on whether the consensus is actually wrong, and then having the patience (and humility) to make a bet - and sit with it - before the rest of the market catches up.

There is no formula for this.

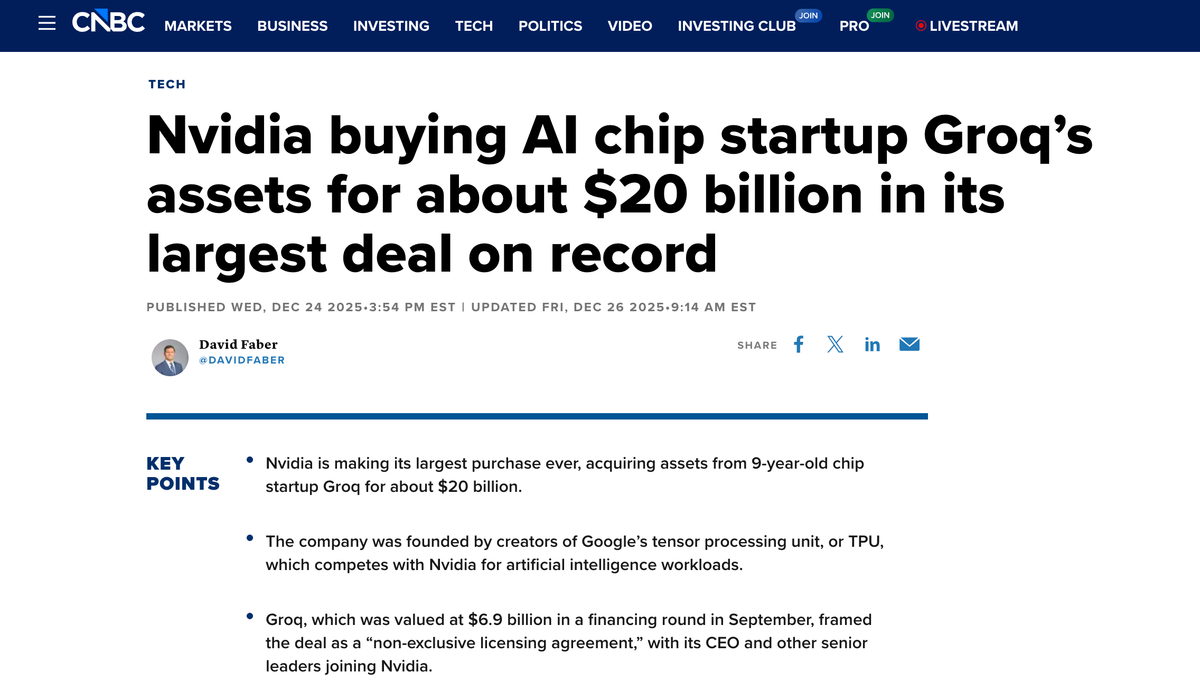

My Series A and B investments in Groq exemplify this.

It’s 2017: most of the tech world is obsessed with Crypto, after Bitcoin hits $20K. AI was beyond unpopular - it wasn’t even considered. But I saw three inflection points converging:

- “Attention is All You Need” was published and showed that machines were truly starting to understand language, heretofore considered the holy grail path to real AI.

- Nvidia's revenue jumped from ~$5bn to $6.9bn from FY 2016 (ending Jan 2016) to FY 2017 (ending Jan 2017), with gaming and crypto mining grabbing headlines. But the hidden story was Data Center revenue surging 144% YoY, from $339M to $830M and on track to grow ~129% to ~$1.9bn in the FY year ending Jan 2018, fueled by the new Volta architecture, purpose-built for AI workloads.

- Hyperscalers like Google were starting to build their own custom chips to train AI models.

It felt like AI was entering a new phase. So, I tried to meet as many people working on this set of problems, as I could.

Lucky for me, one of these people was Jonathan Ross.

At the time, I was a General Partner at Social Capital, and Jonathan was actually already a Social Capital portfolio company founder. Chamath Palihapitiya who ran the firm, had met him mid-2016 (brilliant sourcing), and with no product or even team, had written him a $10M Seed check.

When I sought out Jonathan in mid-2017 to dig into what he was building, I understood why Chamath had been that impressed. He was brilliant, obsessed and had a track record of building cutting edge hardware.

What intrigued me the most, though, was that he had a contrarian vision. He didn't recognize just that AI was accelerating, but that the best way to address compute needs in AI was to build chips that optimized for inference i.e. when a trained neural network use what it has learned to make predictions in real-time.

This was squarely opposed to where Nvidia, the market giant was playing, in building chips for training models - and where the revenue dollars were, at the time.

Back in 2017, it was hard to imagine the plethora of applications that would eventually be built on top of machine learning models. There was no such thing, yet, as foundation models, and no AI APIs, let alone apps like ChatGPT. But my view has always been that AI products would have to be both highly useful and highly usable to gain traction i.e. we needed to design AI for the Real World, as I called it.

I remember sitting in a conference room for over 6 hours, while Jonathan, and cofounder Doug Wightman explained that not only would they focus on inference, but that they would build chips that were more flexible, cheaper to build and easier to use, by doing the following:

- Enabling developers to use high level programming languages to program their chips, so developers would not have to learn special code to run inference applications.

- Building a compiler that could allow anyone to run any machine learning models on its chips with little to no custom optimization required

- Using off-the-shelf hardware components vs cutting edge but niche components.

If someone had no perspective on hardware and/or AI, Jonathan and Doug would’ve sounded nuts. But, there was consistent logic in their story of how to get “from here to there,” that one could actually diligence. I spoke to folks at Nvidia, AMD, and Google, as well as the potential customers for a Groq chip like Amazon and Meta. I had been Head of Product at a datacenter networking company that we sold to Cisco in 2004, and had built custom ASICs, so I was also able to do diligence with a variety of chip manufacturers.

What Groq was proposing was actually feasible, and if they could pull it off, the demand was there.

This gave me the conviction to propose that we actually pre-empt the next round of Groq, before they hit any externally understandable milestones. We convinced Jonathan and Doug that they could accelerate by taking money before they truly needed it, and we ended up investing almost $60M over 2 rounds. Before they ever shipped a single chip.

Peter Thiel calls the vision that the Groq team had "secrets" - founder insights the world thinks are wrong but prove accurate. VCs need these, too, - thesis-driven conviction and a knowledge of under-the radar market opportunities. It is another way to evaluate founders, especially when technology, talent, and business models are shifting this fast. Otherwise, you get lost in all the noise…

We'll be wrong often. But when we're right, it looks like this:

Have a contrarian view on where AI is going? Let's talk!